You need cash fast. Your business is up and running, opportunities are popping up, and you’re ready to scale. You fill out a loan application… and you wait. Days go by. Sometimes weeks.

Why so many delays when some entrepreneurs get approved the same day?

The answer is simple: it’s not the lenders who are slow. It’s incomplete applications, avoidable red flags, and common mistakes that hold up the whole process.

The good news? Every single one of these mistakes can be fixed. And when you have a strong application, approval can happen in hours, not weeks. Here’s exactly what’s slowing down your application—and how to speed things up.

Error #1: You mix your personal and professional finances

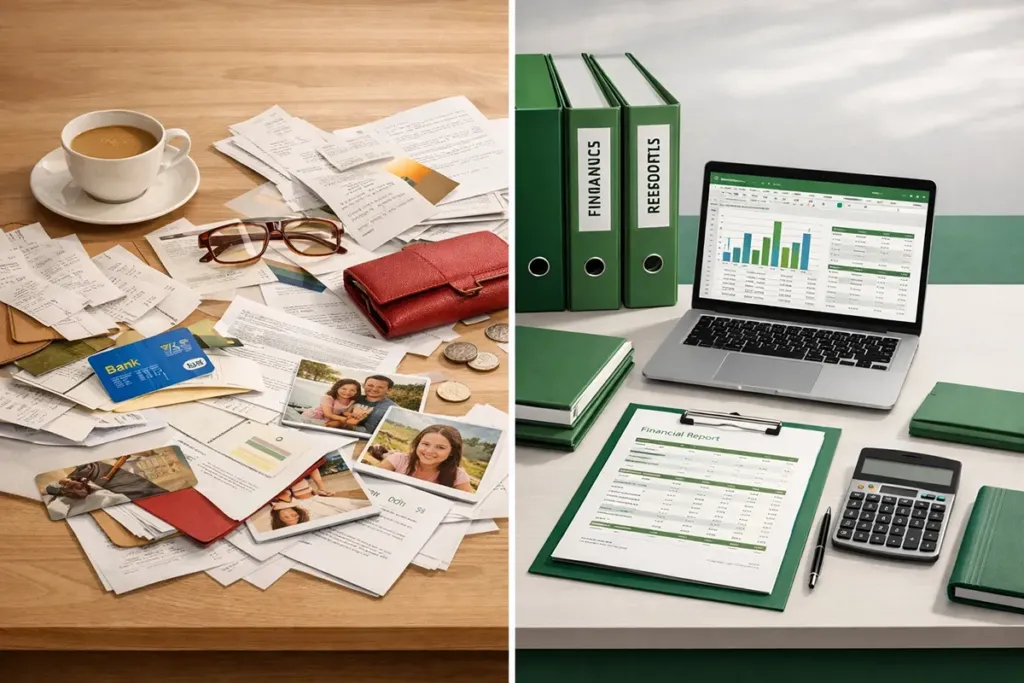

This is the most common mistake Canadian entrepreneurs make, especially in the early years of operation. You use your personal credit card for a business purchase.

You transfer money from your personal account to your business account. It seems convenient.

But for a lender? It’s an analytical nightmare.

When your finances are intertwined, it becomes impossible to determine the true financial health of your business. Is your actual revenue $120,000 or $180,000? Are your operating expenses $40,000, or do they include personal expenses?

How to avoid it:

Open a separate business bank account today

• Get a credit card dedicated solely to business expenses

• Pay yourself a fixed salary instead of random deductions

• Keep separate receipts and a clean accounting system

Lenders like Jetmark Capital can process your application the same day — but only if your financial statements tell a clear story

Error #2: You did not build a commercial credit profile

Your personal credit score is 720. Excellent. But what about your business credit? If you’ve never established a business credit report in Canada, you’re starting from scratch in the eyes of credit bureaus. And even if your business generates $200,000 in annual revenue, without a documented business credit history, you look like a startup.

How to avoid it:

• Register your business with Equifax Canada and Dun & Bradstreet

• Apply for a business credit card and use it regularly (always pay the balance in full)

• Establish business accounts with your key suppliers

• Ensure your supplier payments are reported to the credit bureaus

At Jetmark Capital, we accept businesses with a personal credit score of 500+, but

a strong business credit profile significantly speeds up the approval process

Error #3: Your payments are irregular or overdue

An occasional late payment might seem minor in the daily chaos of running a business. You were out of town. You forgot. The wire transfer took longer than expected.

But to a credit scoring algorithm? It’s a flashing red flag. Every late payment remains on your record for years and can drop your credit score by 20 to 50 points in one fell swoop. Multiply that by three or four incidents, and you’ve just turned a request that would have taken 24 hours into a case requiring weeks of manual review.

How to avoid it:

• Set up automatic payments for all your critical accounts

• Add reminders to your calendar three days before each due date

• Always maintain a cash buffer to cover your minimum payments

• If you anticipate a delay, contact your creditor BEFORE the due date

Error #4: Your credit usage is maximized

You have a $50,000 credit limit and you’re using $48,000. Technically, you’re within the limits. But your utilization ratio is 96%. Lenders interpret this as a sign of financial stress—even if your business is profitable. A high ratio suggests you’re constantly living at the limit of your credit capacity, which raises the question: can you handle another loan?

How to avoid it:

• Keep your credit utilization ratio below 30% of your available credit.

• If you need to use more, request a credit limit increase BEFORE maximizing your current credit.

• Pay off large balances before applying for new financing.

• Diversify your credit sources rather than relying on a single card. Jetmark Capital evaluates your application as a whole—not just your credit utilization—but a healthy ratio always speeds up the process.

Error #5: You are multiplying funding requests in burst

Your traditional bank rejects you. So you immediately apply to three other institutions. Then two more the following week. Each application triggers a thorough investigation of your credit file, and these investigations quickly pile up. When a new lender reviews your history and sees eight applications in two months, they wonder: why doesn’t anyone want to finance me?

How to avoid it:

• Do your research BEFORE applying — identify lenders that match your profile

• Leave at least 30 days between applications if the first one is declined

• Use pre-qualification tools that only generate a light survey

• Work with a specialized lender from the start rather than trying traditional banks

That’s exactly why Jetmark Capital exists. We specialize in fast financing for established Canadian businesses. If you meet our criteria (6 months in operation, $120,000 in annual revenue, 500+ credit score), you get a response the same day. No need to go to ten institutions.

Error #6: Your folder lacks documentation strategic

You fill out the online form. You attach your latest bank statements. And you click “Submit.”

But where is your plan for using the funds? Your financial projections? The proof that this money will generate a return on investment?

Without a strategic context, your application looks like all the others. And generic applications take longer to evaluate because the lender has to guess your intentions.

How to avoid it:

Write a simple plan explaining exactly how you will use the funds.

• Include realistic projections showing the expected impact on your revenue.

• Provide evidence of customer orders, signed contracts, or concrete opportunities.

• Anticipate the lender’s questions and answer them in advance in your application.

At Jetmark Capital, our process is simple and transparent. But a well-prepared application turns a “quick” approval into an “immediate” approval.

Error #7: You are asking for funding for the bad assets

You want a loan to finance an innovative marketing campaign. Or to develop new proprietary software. Or to build a team before launching a product.

These are legitimate investments. But many traditional lenders only finance tangible assets they can secure against: equipment, inventory, commercial real estate. Applying for intangible financing from the wrong type of lender will automatically slow down your application—or lead to a rejection.

How to avoid it:

• First, identify WHAT type of asset or need you are financing.

• Then, choose the appropriate TYPE of financing (secured loan, line of credit, working capital financing, etc.).

• Work with lenders who specialize in your specific need category.

• Be transparent about the intended use of the funds from the outset.

Jetmark Capital specializes in working capital, inventory, and equipment financing for established businesses. We understand your real needs—not just traditional checkboxes.

Your next request may be different

These seven mistakes slow down thousands of Canadian businesses every year. But now that you know them, you won’t be part of that statistic.

A clean file. Separate finances. A solid payment history. A strategic application.

That’s all that separates 24-hour approval from a weeks-long wait.

You’re an established business. You generate revenue. You have a plan. You deserve a financial partner who understands your reality—and moves at your pace.

Jetmark Capital finances Canadian businesses that are building, growing, and need a fast partner. Same-day approval. Funding in less than 24 hours. Simple, transparent process.

No guesswork. No endless waiting. Just the funds you need to seize your next opportunity.