You’re ready to take your business to the next level. The customers are there, the opportunities are there, and you have a solid plan for expansion.

But here’s the question that’s keeping you up at night: which type of financing should you choose? Term loan or line of credit? Both options seem valid. Both have their advantages. And honestly, both can transform your small business… if you choose the right one.

Take a breath. Let’s analyze this together.

Because beyond the technical jargon and bank documents, there’s a simple truth: the right financing isn’t the one that gives you the most money, but the one that aligns with your actual expansion strategy.

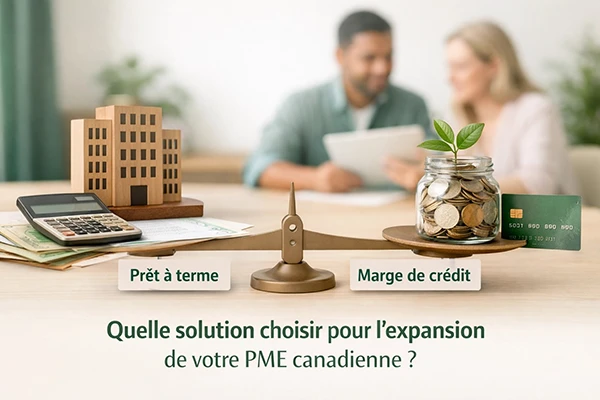

Understanding the fundamentals: what each option means really

Term Loans: Your Ally for Major Investments

A term loan is like building on solid foundations. You receive a fixed sum that you repay according to a precise schedule, with predictable monthly payments.

This is the financing you choose when you know exactly what you want to achieve. New equipment that will double your production capacity? A term loan. Buying commercial premises to consolidate your operations? A term loan. Technology that will

transform your service? Another term loan.

The advantages are clear:

- Total predictability: you know every payment, every due date, every cost

- Interest rates generally lower than other financing options

- Fixed rate that protects you against market fluctuations

- Significant amounts available for major investments

The line of credit: your flexible safety net

A line of credit is your financial cushion. It’s access to funds you use only when you need them, and you only pay interest on what you actually use.

Think of it as an oxygen tank to navigate the unpredictable waters of growth. Orders arriving faster than expected? You tap into your line of credit. A supplier offering a discount for immediate payment? You have the cash flow. An opportunity arising outside the initial plan? You’re ready.

Game-changing benefits:

- Maximum flexibility: Use what you need, when you need it.

- Repayment at your own pace: No fixed principal repayment obligation.

- Immediate access to funds to seize opportunities quickly.

- Proportional costs: You only pay for what you use.

Quelle option pour quelle extension ? Voici comment décider intelligemment

The question is not ‘which is the best?’ but rather ‘which one corresponds to your type of expansion?

Choose the term loan if...

Your expansion is structured and defined. You have a precise plan, clear figures, and a calculated return on investment.

Concrete examples:

- You purchase equipment that costs $150,000 and will generate an additional $50,000 in revenue per year

- You renovate your retail space to accommodate more customers or employees

- You invest in new technology that will transform your operations

- You consolidate several high-interest debts into a single, predictable payment

A term loan is your best friend when you can draw a straight line between the investment and the expected results.

Choose the line of credit if...

Your expansion is dynamic and evolving. You know you’re going to grow, but your specific needs vary month after month. Here are some telling examples:

Your business is seasonal, and you have to manage significant cash flow fluctuations.

You need to maintain a larger inventory to meet increasing demand.

You’re hiring quickly and need to cover payroll during the ramp-up period.

You’re negotiating with multiple suppliers and need the ability to seize the best opportunities.

A line of credit is your strategic weapon when flexibility is more important than predictability.

What traditional institutions do not tell you

Here’s the reality: traditional banks love businesses that fit their formulas. A small business with at least three years of history? Excellent credit rating? Substantial personal guarantees? Welcome to the club.

But what if your business is growing rapidly? What if your cash flow is strong but irregular? What if you’re building something different that doesn’t fit their mold?

This is where many Canadian entrepreneurs hit a wall. Not because their project

is not solid. Not because their strategy is not brilliant. Simply because the traditional system is not designed for the reality of modern entrepreneurial growth.

The Jetmark Capital approach: financing that adapts to you

At Jetmark Capital, we don’t ask you to fit into a mold. We analyze your business as it is: with its strengths, its potential, and its actual trajectory.

Our approach is a game changer:

24-hour approval – because expansion opportunities don’t wait for weeks of bureaucratic processes. You submit your application, we quickly analyze your cash flow and situation, and we give you a clear answer.

Based on your revenue, not just your history – your business generates strong sales but you’ve only been in operation for 18 months? We look at your current performance, not just the time elapsed.

Flexibility tailored to your reality – need a term loan for specific equipment? We can do that. Need a hybrid solution that combines stability and flexibility? We’ll build that with you.

The winning strategy: combining the two

Here’s what the most strategic entrepreneurs understand: you don’t have to choose just one option.

The most powerful combination? A term loan to finance your major expansion investments + a line of credit to manage your day-to-day operations.

What does that look like in practice?

- You use a $200,000 term loan to purchase the equipment that will double your production capacity. Fixed payments, predictable interest rate, clear plan.

- You establish a $50,000 line of credit to manage cash flow fluctuations while you ramp up with this new equipment.

The result?

You have the financial stability for your major investment AND the flexibility to navigate the unexpected challenges of growth.

Canadian government programs: what is needed savoir

The Canada Small Business Financing Program (CSBF) can offer up to $1,000,000 in term loans—a substantial amount for serious expansion.

But pay attention to the details:

- Maximum of $500,000 for equipment and leasehold improvements

- Only $150,000 available as a line of credit

- Specific eligibility criteria that may not be suitable for all SMEs

It’s definitely an option to consider. But it’s not your only avenue if it doesn’t apply to your situation.

Your next three concrete actions

First step: Clearly define your expansion needs. Write it down: how much do you need, for what exactly, and what is your expected return on investment?

Second step: Analyze your cash flow over the last 12 months. Identify periods of high and low cash flow. This will tell you whether you need flexibility (line of credit) or stability (term loan).

Third step: Contact Jetmark Capital for a quick, no-obligation assessment. Within 24 hours, you’ll know exactly what options are available to you and how to structure your financing intelligently.

The truth about successful expansion

Here’s what 15 years in commercial finance has taught us: expansion doesn’t rewardthose who wait for perfect conditions, but those who act with the rightresources at the right time.

Financing isn’t an obstacle to overcome. It’s a strategic lever to activate.

Term loan, line of credit, or a combination of both – the right answer is the one that allows you to execute your vision without compromising your financial stability.

At Jetmark Capital, we don’t finance dreams. We finance entrepreneurs who have a plan, a clear vision, and the determination to build something sustainable in the Canadian market.

Your expansion awaits. Financing shouldn’t be what holds you back.